Introduction to kardl

Huseyin karamelikli and Huseyin Utku Demir

2026-07-21

Source:vignettes/intro.Rmd

intro.RmdIntroduction

The kardl package is an R tool for estimating symmetric

and asymmetric Autoregressive Distributed Lag (ARDL) and Nonlinear ARDL

(NARDL) models, designed for econometricians and researchers analyzing

cointegration and dynamic relationships in time series data. It offers

flexible model specifications, allowing users to include deterministic

variables, asymmetric effects for short- and long-run dynamics, and

trend components. The package supports customizable lag structures,

model selection criteria (AIC, BIC, AICc, HQ), and parallel processing

for computational efficiency. Key features include:

-

Flexible Formula Specification: Use

asymmetric(),lasymmetric(), andsasymmetric()to model asymmetric effects in short- and long-run dynamics, anddeterministic()for dummy variables. -

Lag Optimization: Choose between automatic lag

selection (

"quick","grid","grid_custom") or user-defined lags. - Dynamic Analysis: Compute long-run coefficients, perform cointegration tests (PSS F, PSS t, Narayan), and ECM estimation.

This vignette demonstrates how to use the kardl()

function to estimate an asymmetric ARDL model, perform diagnostic tests,

and visualize results, using economic data from Turkey.

Installation

kardl in R can easily be installed from its CRAN

repository:

install.packages("kardl")

library(kardl)Alternatively, you can use the devtools package to load

directly from GitHub:

# Install required packages

install.packages(c(

"stats", "msm", "lmtest", "nlWaldTest", "car", "strucchange",

"utils", "ggplot2"

))

# Install kardl from GitHub

install.packages("devtools")

devtools::install_github("karamelikli/kardl")Load the package:

Unique Features and Methodological Contributions

The kardl package implements several methodological

extensions and improvements for ARDL/NARDL modelling that go beyond

standard implementations available in R and other software:

- different_asym_lag option: Enables different lag orders for the positive and negative partial sum decompositions in NARDL models. This provides greater flexibility than the common symmetric lag restriction used in most existing packages.

-

Narayan cointegration test

(

narayan()): A dedicated small-sample bounds test (Narayan, 2005) with automatic handling of critical values for cases II–V. While the test exists in the literature, its seamless integration into a full ARDL/NARDL workflow is unique in R. -

Symmetry tests (

symmetrytest()): Comprehensive Wald tests for both short-run and long-run symmetry in NARDL models. - Bootstrap confidence intervals for dynamic multipliers: Robust uncertainty quantification around short-run, long-run, and impact multipliers through resampling methods, fully integrated with asymmetric multiplier estimation.

- Additional advanced capabilities include highly flexible formula parsing for mixed symmetric/asymmetric regressors, multiple model selection criteria (AIC, BIC, AICc, HQ), parallel processing support, and extensive post-estimation tools tailored for asymmetric analysis.

These features make kardl particularly suitable for

researchers needing fine-grained control over asymmetric dynamics and

small-sample inference.

Estimating an asymmetric ARDL Model

This example estimates an asymmetric ARDL model to analyze the impact

of petrol prices and driving patterns on road fatalities in the UK,

using the built-in Seatbelts dataset with variables for

DriversKilled, PetrolPrice, drivers, kms, and a seatbelt law dummy

variable.

Step 1: Data Preparation

The Seatbelts dataset contains monthly data on road

casualties in Great Britain from 1969 to 1984. We convert it to a data

frame for analysis.

Note: The Seatbelts dataset is a built-in R dataset

included in the datasets package. The data can be accessed

directly by converting the time series object to a data frame.

Step 2: Define the Model Formula

We define the model formula using R’s formula syntax, incorporating

asymmetric effects and deterministic variables. We use

asymmetric() for variables with both short- and long-run

asymmetry, lasymmetric() for long-run asymmetry,

sasymmetric() for short-run asymmetry, and

deterministic() for fixed dummy variables. The

trend term includes a linear time trend in the model.

# Define the model formula

my_formula <- DriversKilled ~ PetrolPrice + drivers +

asymmetric(PetrolPrice + drivers) + deterministic(law) + trendIndeed, the formula syntax is flexible, allowing for various combinations of asymmetric and deterministic variables. The following variations of the formula are equivalent and will yield the same model specification:

same_formula <- y ~ asymmetric(x1) +

sasymmetric(x2 + x3) +

lasymmetric(x4 + x5) +

deterministic(dummy1) + trend

same_formula <- y ~ asymmetric(x1) +

sasymmetric(x2 + x3) +

lasymmetric(x4 + x5) +

deterministic(dummy1) + trend

same_formula <- y ~ asym(x1) + sasym(x2 + x3) + lasym(x4 + x5) +

det(dummy1) + trend

same_formula <- y ~ a(x1) + s(x2 + x3) + l(x4 + x5) + d(dummy1) + trendStep 3: Model Estimation

We estimate the ARDL model using different mode settings

to demonstrate flexibility in lag selection. The kardl()

function supports various modes: "grid",

"grid_custom", "quick", or a user-defined lag

vector.

Using mode = "grid"

The "grid" mode evaluates all lag combinations up to

maxlag and provides console feedback.

# Set model options

kardl_set(criterion = "BIC", different_asym_lag = TRUE, data = Seatbelts)

# Estimate model with grid mode

kardl_model <- kardl(

data = Seatbelts, formula = my_formula,

maxlag = 4, mode = "grid"

)

# View results

kardl_model## Optimal lags for each variable ( BIC ):

##

## DriversKilled: 1, PetrolPrice_POS: 0, PetrolPrice_NEG: 0, drivers_POS: 0, drivers_NEG: 0

##

##

## Call:

## lm(formula = my_formula, data = model_data)

##

## Coefficients:

## (Intercept) L1.DriversKilled L1.PetrolPrice_POS

## 134.84809 -1.11975 -58.85309

## L1.PetrolPrice_NEG L1.drivers_POS L1.drivers_NEG

## -43.01060 0.08228 0.08886

## L1.d.DriversKilled L0.d.PetrolPrice_POS L0.d.PetrolPrice_NEG

## 0.13726 -285.05578 1028.03999

## L0.d.drivers_POS L0.d.drivers_NEG law

## 0.07562 0.07997 -0.61874

## trend

## 0.63798Summary of the model provides detailed information about the estimated coefficients, standard errors, t-values, and significance levels.

# Display model summary

summary(kardl_model)##

## Call:

## lm(formula = my_formula, data = model_data)

##

## Residuals:

## Min 1Q Median 3Q Max

## -27.425 -7.449 -1.070 7.966 34.134

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 1.348e+02 1.151e+01 11.720 < 2e-16 ***

## L1.DriversKilled -1.120e+00 8.866e-02 -12.630 < 2e-16 ***

## L1.PetrolPrice_POS -5.885e+01 9.949e+01 -0.592 0.55489

## L1.PetrolPrice_NEG -4.301e+01 1.633e+02 -0.263 0.79252

## L1.drivers_POS 8.228e-02 9.405e-03 8.748 1.66e-15 ***

## L1.drivers_NEG 8.886e-02 8.341e-03 10.653 < 2e-16 ***

## L1.d.DriversKilled 1.373e-01 4.699e-02 2.921 0.00394 **

## L0.d.PetrolPrice_POS -2.851e+02 3.313e+02 -0.860 0.39069

## L0.d.PetrolPrice_NEG 1.028e+03 9.132e+02 1.126 0.26179

## L0.d.drivers_POS 7.562e-02 8.643e-03 8.750 1.65e-15 ***

## L0.d.drivers_NEG 7.997e-02 7.494e-03 10.672 < 2e-16 ***

## law -6.187e-01 4.503e+00 -0.137 0.89086

## trend 6.380e-01 5.028e-01 1.269 0.20620

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 11.36 on 177 degrees of freedom

## (2 observations deleted due to missingness)

## Multiple R-squared: 0.7486, Adjusted R-squared: 0.7316

## F-statistic: 43.93 on 12 and 177 DF, p-value: < 2.2e-16Using User-Defined Lags

Specify custom lags to bypass automatic lag selection:

kardl_model2 <- kardl(

data = Seatbelts, my_formula,

mode = c(2, 1, 1, 3, 0)

)

# View results

kardl_extract(kardl_model2, "opt_lag")## DriversKilled PetrolPrice_POS PetrolPrice_NEG drivers_POS drivers_NEG

## 2 1 1 3 0

# Display model summary

summary(kardl_model2)##

## Call:

## lm(formula = my_formula, data = model_data)

##

## Residuals:

## Min 1Q Median 3Q Max

## -26.5337 -7.5749 -0.5198 7.5158 31.0525

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 1.297e+02 1.462e+01 8.873 1.03e-15 ***

## L1.DriversKilled -1.077e+00 1.060e-01 -10.159 < 2e-16 ***

## L1.PetrolPrice_POS -8.365e+01 1.167e+02 -0.717 0.4744

## L1.PetrolPrice_NEG -4.826e+01 1.801e+02 -0.268 0.7891

## L1.drivers_POS 7.411e-02 1.255e-02 5.904 1.92e-08 ***

## L1.drivers_NEG 8.073e-02 1.019e-02 7.926 3.00e-13 ***

## L1.d.DriversKilled 1.281e-01 6.923e-02 1.851 0.0660 .

## L2.d.DriversKilled 7.203e-02 5.195e-02 1.387 0.1674

## L0.d.PetrolPrice_POS -3.189e+02 3.390e+02 -0.941 0.3482

## L1.d.PetrolPrice_POS -5.298e+01 3.639e+02 -0.146 0.8844

## L0.d.PetrolPrice_NEG 7.248e+02 9.573e+02 0.757 0.4500

## L1.d.PetrolPrice_NEG 6.564e+01 8.720e+02 0.075 0.9401

## L0.d.drivers_POS 7.499e-02 8.845e-03 8.478 1.12e-14 ***

## L1.d.drivers_POS 1.236e-02 1.272e-02 0.972 0.3327

## L2.d.drivers_POS -1.852e-02 1.111e-02 -1.668 0.0972 .

## L3.d.drivers_POS 7.892e-03 9.504e-03 0.830 0.4075

## L0.d.drivers_NEG 7.555e-02 7.797e-03 9.689 < 2e-16 ***

## law -1.353e+00 5.002e+00 -0.270 0.7871

## trend 6.507e-01 5.907e-01 1.101 0.2723

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 11.31 on 168 degrees of freedom

## (5 observations deleted due to missingness)

## Multiple R-squared: 0.7601, Adjusted R-squared: 0.7344

## F-statistic: 29.57 on 18 and 168 DF, p-value: < 2.2e-16Using All Variables

Use the . operator to include all variables except the

dependent variable:

## Optimal lags for each variable ( BIC ):

##

## DriversKilled: 1, drivers: 0, front: 0, rear: 0, kms: 0, PetrolPrice: 0, VanKilled: 0

##

##

## Call:

## lm(formula = my_formula, data = model_data)

##

## Coefficients:

## (Intercept) L1.DriversKilled L1.drivers L1.front

## -5.480e+00 -1.107e+00 8.236e-02 3.755e-03

## L1.rear L1.kms L1.PetrolPrice L1.VanKilled

## -5.576e-03 4.442e-04 -5.069e+01 1.232e-01

## L1.d.DriversKilled L0.d.drivers L0.d.front L0.d.rear

## 1.380e-01 7.928e-02 -5.884e-04 -6.872e-03

## L0.d.kms L0.d.PetrolPrice L0.d.VanKilled law

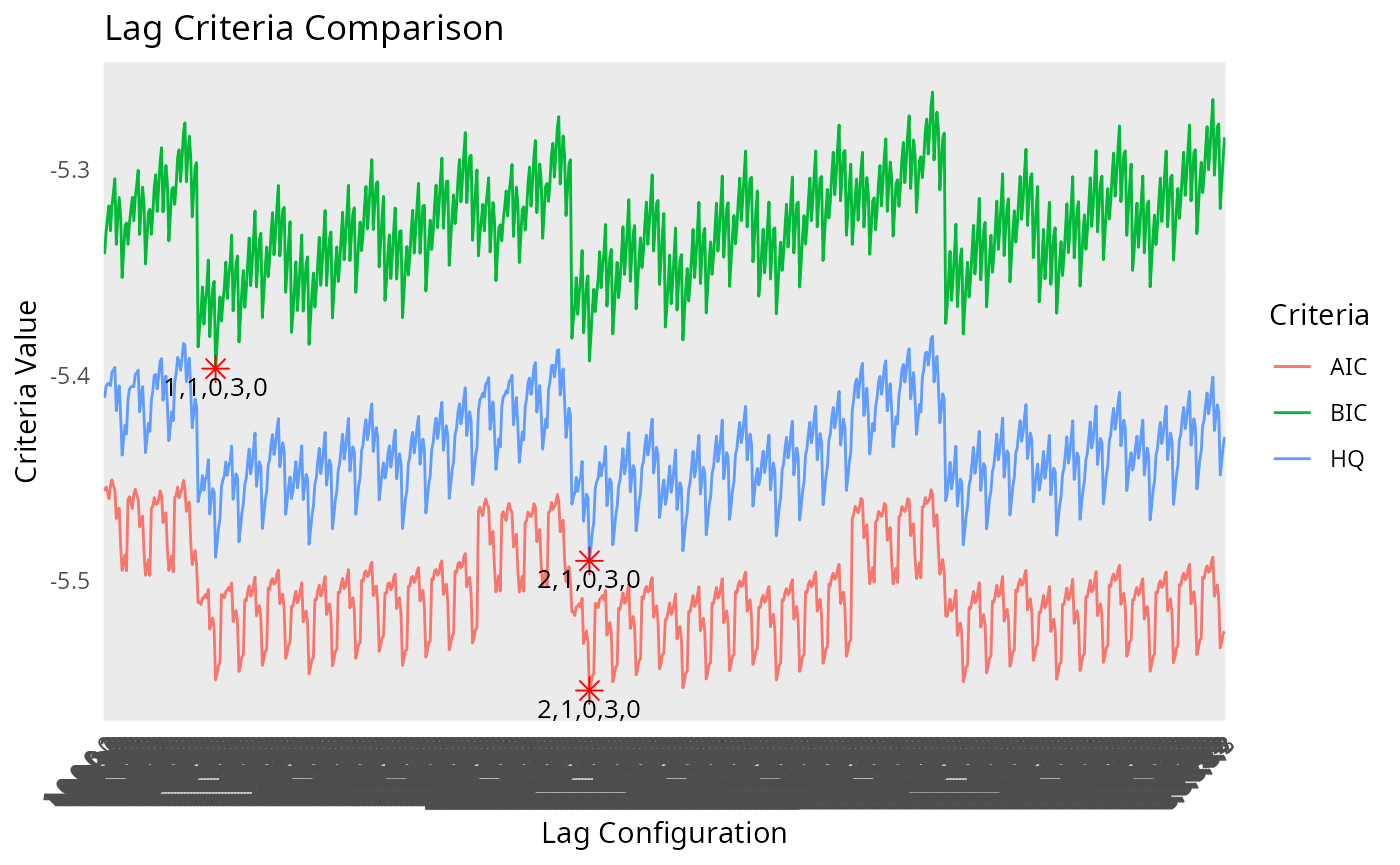

## -7.470e-04 -3.693e+01 -1.215e-01 4.680e+00Visualizing Lag Criteria

The lag_criteria component contains lag combinations and

their criterion values. We visualize these to compare model selection

criteria (AIC, BIC, HQ).

library(dplyr)

library(tidyr)

library(ggplot2)

# Convert lag_criteria to a data frame

lag_criteria <- as.data.frame(kardl_extract(kardl_model, "lag_criteria"))

lag_criteria <- lag_criteria |> mutate(across(c(AIC, BIC, HQ), as.numeric))

# Pivot to long format

lag_criteria_long <- lag_criteria |>

select(-c(AICc, AdjR2)) |>

pivot_longer(

cols = c(AIC, BIC, HQ),

names_to = "Criteria",

values_to = "Value"

)

# Find minimum values

min_values <- lag_criteria_long |>

group_by(Criteria) |>

slice_min(order_by = Value) |>

ungroup()

# Plot

ggplot(

lag_criteria_long,

aes(x = lag, y = Value, color = Criteria, group = Criteria)

) +

geom_line() +

geom_point(

data = min_values, aes(x = lag, y = Value),

color = "red", size = 3, shape = 8

) +

geom_text(

data = min_values, aes(x = lag, y = Value, label = lag),

vjust = 1.5, color = "black", size = 3.5

) +

scale_x_discrete(

breaks = lag_criteria$lag[seq(1, nrow(lag_criteria), by = 20)]

) +

labs(

title = "Lag Criteria Comparison",

x = "Lag Configuration",

y = "Criteria Value"

) +

theme_minimal() +

theme(axis.text.x = element_text(angle = 45, hjust = 1))

Error Correction Model (ECM) Estimation

The ecm() function estimates a Restricted ECM for

cointegration testing. We specify the same formula and lag structure as

in the ARDL model.

ecm_model <- ecm(

data = Seatbelts, formula = my_formula,

maxlag = 4, mode = "grid_custom"

)

# View results

summary(ecm_model)##

## Call:

## lm(formula = shortrun_eq, data = ecm_data)

##

## Residuals:

## Min 1Q Median 3Q Max

## -28.232 -7.445 -0.876 7.570 34.774

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 1.882e+00 2.152e+00 0.875 0.38295

## EcmRes -1.116e+00 8.791e-02 -12.691 < 2e-16 ***

## L1.d.DriversKilled 1.279e-01 4.407e-02 2.903 0.00415 **

## L0.d.PetrolPrice_POS -1.892e+02 3.158e+02 -0.599 0.54987

## L0.d.PetrolPrice_NEG 8.670e+02 8.224e+02 1.054 0.29322

## L0.d.drivers_POS 7.794e-02 8.380e-03 9.300 < 2e-16 ***

## L0.d.drivers_NEG 8.337e-02 6.251e-03 13.338 < 2e-16 ***

## law 3.554e+00 3.218e+00 1.104 0.27088

## trend -7.841e-03 1.873e-02 -0.419 0.67599

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 11.3 on 181 degrees of freedom

## Multiple R-squared: 0.7455, Adjusted R-squared: 0.7342

## F-statistic: 66.27 on 8 and 181 DF, p-value: < 2.2e-16Step 4: Long-Run Coefficients

We calculate long-run coefficients using

kardl_longrun(), which standardizes coefficients by

dividing them by the negative of the dependent variable’s long-run

parameter.

# Long-run coefficients

my_long <- kardl_longrun(kardl_model)

my_long##

## Call:

## kardl_longrun.kardl_lm(kardl_model = kardl_model)

##

## Coefficients:

## L1.PetrolPrice_POS L1.PetrolPrice_NEG L1.drivers_POS L1.drivers_NEG

## -52.55915 -38.41091 0.07348 0.07935The summary() function provides detailed information

about the long-run coefficients, including standard errors, t-values,

and significance levels.

# Summary of long-run coefficients

summary(my_long)## Call:

## kardl_longrun.kardl_lm(kardl_model = kardl_model)

##

##

## Estimation type:

## Long-run multipliers

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## L1.PetrolPrice_POS -52.5591494 88.7809404 -0.5920 0.5546

## L1.PetrolPrice_NEG -38.4109100 145.6977929 -0.2636 0.7924

## L1.drivers_POS 0.0734767 0.0056809 12.9340 <2e-16 ***

## L1.drivers_NEG 0.0793527 0.0041634 19.0594 <2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1Step 5: Symmetry Test

The symmetrytest() function performs Wald tests to

assess short- and long-run asymmetry in the model.

ast <- Seatbelts |>

kardl(

DriversKilled ~ PetrolPrice + drivers + asymmetric(PetrolPrice + drivers) +

deterministic(law) + trend,

mode = c(1, 2, 3, 0, 1),

data = _

) |>

symmetrytest()

ast## kardl Symmetry Test

##

## Long-run:

## Df Sum of Sq Mean Sq F value Pr(>F)

## PetrolPrice 1 2.663 2.663 0.020 0.8877

## drivers 1 175.149 175.149 1.316 0.2530

##

## Short-run:

## Df Sum of Sq Mean Sq F value Pr(>F)

## PetrolPrice 1 2.649 2.649 0.0199 0.8880

## drivers 1 35.235 35.235 0.2647 0.6076Summary of the symmetry test provides detailed results for both long-run and short-run asymmetry tests, including F-values, p-values, hypotheses, and test decisions.

# Summary of symmetry test

summary(ast)## Symmetry Test Summary

##

## Long-run:

## Df Sum of Sq Mean Sq F value Pr(>F)

## PetrolPrice 1 2.663 2.663 0.020 0.8877

## drivers 1 175.149 175.149 1.316 0.2530

##

## Hypotheses:

##

## PetrolPrice

## H0: - Coef(L1.PetrolPrice_POS)/Coef(L1.DriversKilled) = - Coef(L1.PetrolPrice_NEG)/Coef(L1.DriversKilled)

## H1: At least one coefficient differs from zero.

## Decision: Fail to Reject H0 at 5% level. Indicating long-run symmetry for variable PetrolPrice.

##

## drivers

## H0: - Coef(L1.drivers_POS)/Coef(L1.DriversKilled) = - Coef(L1.drivers_NEG)/Coef(L1.DriversKilled)

## H1: At least one coefficient differs from zero.

## Decision: Fail to Reject H0 at 5% level. Indicating long-run symmetry for variable drivers.

##

##

## Short-run:

## Df Sum of Sq Mean Sq F value Pr(>F)

## PetrolPrice 1 2.649 2.649 0.0199 0.8880

## drivers 1 35.235 35.235 0.2647 0.6076

##

## Hypotheses:

##

## PetrolPrice

## H0: Coef(L0.d.PetrolPrice_POS) + Coef(L1.d.PetrolPrice_POS) + Coef(L2.d.PetrolPrice_POS) = Coef(L0.d.PetrolPrice_NEG) + Coef(L1.d.PetrolPrice_NEG) + Coef(L2.d.PetrolPrice_NEG) + Coef(L3.d.PetrolPrice_NEG)

## H1: Coef(L0.d.PetrolPrice_POS) + Coef(L1.d.PetrolPrice_POS) + Coef(L2.d.PetrolPrice_POS) ≠ Coef(L0.d.PetrolPrice_NEG) + Coef(L1.d.PetrolPrice_NEG) + Coef(L2.d.PetrolPrice_NEG) + Coef(L3.d.PetrolPrice_NEG)

## Decision: Fail to Reject H0 at 5% level. Indicating short-run symmetry for variable PetrolPrice.

##

## drivers

## H0: Coef(L0.d.drivers_POS) = Coef(L0.d.drivers_NEG) + Coef(L1.d.drivers_NEG)

## H1: Coef(L0.d.drivers_POS) ≠ Coef(L0.d.drivers_NEG) + Coef(L1.d.drivers_NEG)

## Decision: Fail to Reject H0 at 5% level. Indicating short-run symmetry for variable drivers.Step 6: Cointegration Tests

We perform cointegration tests to assess long-term relationships

using pssf(), psst(), and

narayan().

PSS F Bound Test

The pssf() function tests for cointegration using the

Pesaran, Shin, and Smith F Bound test.

test_result <- kardl_model |> pssf(case = 3, signif_level = "0.05")

test_result##

## Pesaran-Shin-Smith (PSS) Bounds F-test for cointegration

##

## data: kardl_model

## F = 32.345

## alternative hypothesis: Cointegrating relationship existsSummary of the PSS F Bound test provides detailed information about the test statistic, critical values, hypotheses, and decision regarding cointegration.

summary(test_result)## KARDL Cointegration Test Summary

##

## Pesaran-Shin-Smith (PSS) Bounds F-test for cointegration

##

## F statistic = 32.3445539

##

## Critical Values (Lower & Upper Bounds):

## L U

## 10% 3.03 4.06

## 5% 3.47 4.57

## 2.5% 3.89 5.07

## 1% 4.40 5.72

##

## Decision:

## Reject H0 → Cointegration (at 5% level)

##

## Comparison:

## At the 5% significance level, F (32.3445539) exceeds the upper bound (4.57).

## This indicates that the variables tend to move together over time.

## Conclusion: There is strong evidence of a long-run relationship (cointegration).

##

## Hypotheses:

## H0: Coef(L1.DriversKilled) = Coef(L1.PetrolPrice_POS) = Coef(L1.PetrolPrice_NEG) = Coef(L1.drivers_POS) = Coef(L1.drivers_NEG) = 0

## H1: Not all of Coef(L1.DriversKilled), Coef(L1.PetrolPrice_POS), Coef(L1.PetrolPrice_NEG), Coef(L1.drivers_POS), Coef(L1.drivers_NEG) are zero.

##

## Model Details:

## Number of regressors (k): 4

## Case: VPSS t Bound Test

The psst() function tests the significance of the lagged

dependent variable’s coefficient.

test_result <- kardl_model |> psst(case = 3, signif_level = "0.05")

test_result##

## Pesaran-Shin-Smith (PSS) Bounds t-test for cointegration

##

## data: model

## t = -12.63

## alternative hypothesis: Cointegrating relationship existsSummary of the PSS t Bound test provides detailed information about the test statistic, critical values, hypotheses, and decision regarding cointegration.

summary(test_result)## KARDL Cointegration Test Summary

##

## Pesaran-Shin-Smith (PSS) Bounds t-test for cointegration

##

## t statistic = -12.6296459

##

## Critical Values (Lower & Upper Bounds):

## L U

## 10% -3.13 -4.04

## 5% -3.41 -4.36

## 2.5% -3.65 -4.62

## 1% -3.96 -4.96

##

## Decision:

## Reject H0 → Cointegration (at 5% level)

##

## Comparison:

## At the 5% significance level, t (12.6296459) exceeds the upper bound (4.36).

## This indicates that the variables tend to move together over time.

## Conclusion: There is strong evidence of a long-run relationship (cointegration).

##

## Hypotheses:

## H0: Coef(L1.DriversKilled) = 0

## H1: Coef(L1.DriversKilled) ≠ 0

##

## Model Details:

## Number of regressors (k): 4

## Case: VNarayan Test

The narayan() function is tailored for small sample

sizes. It tests for cointegration using critical values optimized for

small samples.

test_result <- kardl_model |> narayan(case = 3, signif_level = "0.05")

test_result##

## Narayan F Test for Cointegration

##

## data: model

## F = 32.345

## alternative hypothesis: Cointegrating relationship existsSummary of the Narayan test provides detailed information about the test statistic, critical values, hypotheses, and decision regarding cointegration.

summary(test_result)## KARDL Cointegration Test Summary

##

## Narayan F Test for Cointegration

##

## F statistic = 32.3445539

##

## Critical Values (Lower & Upper Bounds):

## L U

## 10% 3.160 4.230

## 5% 3.678 4.840

## 1% 4.890 6.164

##

## Decision:

## Reject H0 → Cointegration (at 5% level)

##

## Comparison:

## At the 5% significance level, F (32.3445539) exceeds the upper bound (4.84).

## This indicates that the variables tend to move together over time.

## Conclusion: There is strong evidence of a long-run relationship (cointegration).

##

## Hypotheses:

## H0: Coef(L1.DriversKilled) = Coef(L1.PetrolPrice_POS) = Coef(L1.PetrolPrice_NEG) = Coef(L1.drivers_POS) = Coef(L1.drivers_NEG) = 0

## H1: Not all of Coef(L1.DriversKilled), Coef(L1.PetrolPrice_POS), Coef(L1.PetrolPrice_NEG), Coef(L1.drivers_POS), Coef(L1.drivers_NEG) are zero.

##

## Model Details:

## Number of regressors (k): 4

## Case: V

##

## Note:

## The number of observations exceeds the maximum limit for the critical values table. Using the critical values for 80 observations.Step 7: Dynamic Multipliers

The mplier() function calculates dynamic multipliers for

the model, showing how changes in independent variables affect the

dependent variable over time.

multipliers <- kardl_model |> mplier()

# View multipliers of the model

head(kardl_extract(multipliers, "multipliers"))## h PetrolPrice_POS PetrolPrice_NEG PetrolPrice_dif drivers_POS drivers_NEG

## [1,] 0 -285.05578 -1028.03999 -1313.095765 0.07562484 -0.07997262

## [2,] 1 -63.84422 25.01033 -38.833893 0.08359961 -0.09025538

## [3,] 2 -20.84449 184.55623 163.711736 0.07335905 -0.07945846

## [4,] 3 -50.45487 42.80916 -7.645706 0.07208514 -0.07785801

## [5,] 4 -56.87543 18.42816 -38.447262 0.07346844 -0.07931196

## [6,] 5 -52.92356 37.45733 -15.466230 0.07366752 -0.07955710

## drivers_dif

## [1,] -0.004347775

## [2,] -0.006655767

## [3,] -0.006099407

## [4,] -0.005772873

## [5,] -0.005843521

## [6,] -0.005889578

# View long-run multipliers

kardl_extract(multipliers, "omega")## [1] 0.01750931 -0.13725897

# View short-run multipliers

head(kardl_extract(multipliers, "lambda"))## PetrolPrice_POS PetrolPrice_NEG drivers_POS drivers_NEG

## [1,] -285.0558 1028.040 0.075624845 0.07997262

## [2,] 226.2027 -1071.051 0.006650624 0.00888249

## [3,] 0.0000 0.000 0.000000000 0.00000000

## [4,] 0.0000 0.000 0.000000000 0.00000000

## [5,] 0.0000 0.000 0.000000000 0.00000000

## [6,] 0.0000 0.000 0.000000000 0.00000000Plotting dynamic multipliers for specific variables can be done using

the plot() function, which visualizes the response of the

dependent variable to changes in independent variables over time.

To handle a large number of variables, you can specify a subset of

variables to plot or use variables = "all" to visualize all

dynamic multipliers.

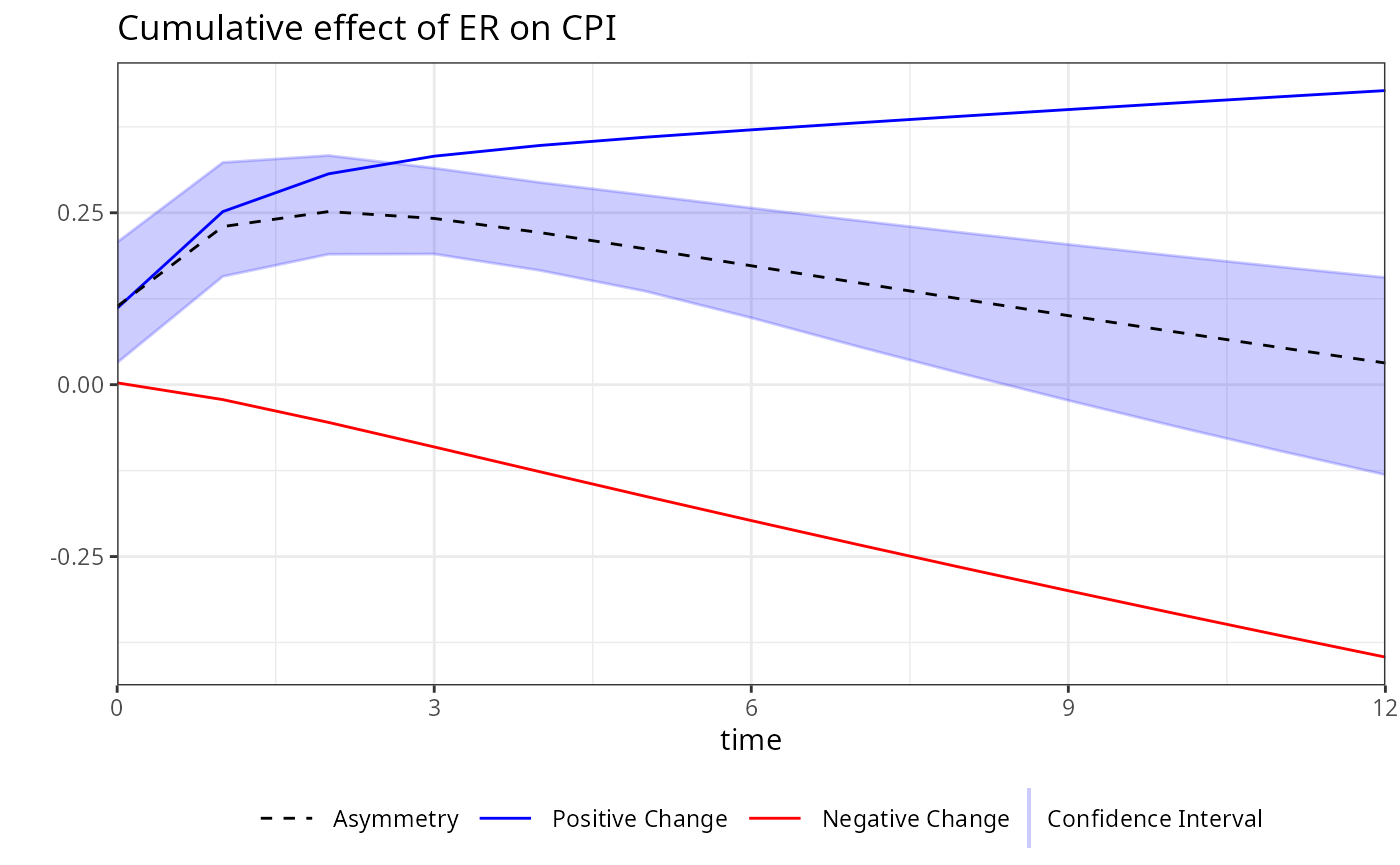

Bootstrap confidence intervals for dynamic multipliers can be

calculated using the bootstrap() function, which provides

robust estimates of uncertainty around the multipliers.

bootstrap_results <- kardl_model |>

bootstrap(horizon = 12, replications = 10)

# View bootstrap summary

summary(bootstrap_results)## Summary of Dynamic Multipliers

## Horizon: 12

##

## h PetrolPrice_POS PetrolPrice_NEG PetrolPrice_dif

## Min. : 0 Min. :-285.06 Min. :-1028.04 Min. :-1313.10

## 1st Qu.: 3 1st Qu.: -52.92 1st Qu.: 37.46 1st Qu.: -15.47

## Median : 6 Median : -52.56 Median : 38.40 Median : -14.16

## Mean : 6 Mean : -69.03 Mean : -34.49 Mean : -103.52

## 3rd Qu.: 9 3rd Qu.: -52.50 3rd Qu.: 38.59 3rd Qu.: -13.91

## Max. :12 Max. : -20.84 Max. : 184.56 Max. : 163.71

## drivers_POS drivers_NEG drivers_dif PetrolPrice_CI_upper

## Min. :0.07209 Min. :-0.09026 Min. :-0.006656 Min. :167.7

## 1st Qu.:0.07347 1st Qu.:-0.07946 1st Qu.:-0.005881 1st Qu.:224.4

## Median :0.07348 Median :-0.07935 Median :-0.005876 Median :225.6

## Mean :0.07432 Mean :-0.08014 Mean :-0.005826 Mean :286.2

## 3rd Qu.:0.07348 3rd Qu.:-0.07935 3rd Qu.:-0.005874 3rd Qu.:233.8

## Max. :0.08360 Max. :-0.07786 Max. :-0.004348 Max. :638.4

## PetrolPrice_CI_lower drivers_CI_upper drivers_CI_lower

## Min. :-3769.4 Min. :-0.0023941 Min. :-0.02943

## 1st Qu.: -299.5 1st Qu.:-0.0021219 1st Qu.:-0.01328

## Median : -298.7 Median :-0.0021181 Median :-0.01327

## Mean : -561.1 Mean :-0.0008551 Mean :-0.01448

## 3rd Qu.: -297.4 3rd Qu.:-0.0021174 3rd Qu.:-0.01323

## Max. : -255.9 Max. : 0.0146270 Max. :-0.01113Visualize bootstrap results for specific variables to understand the variability and confidence intervals of the dynamic multipliers.

plot(bootstrap_results, variables = "drivers")

Step 8: Customizing asymmetric Variables

We demonstrate how to customize prefixes and suffixes for asymmetric

variables using kardl_set().

# Set custom prefixes and suffixes

kardl_reset()

kardl_set(asym_prefix = c("asyP_", "asyN_"), asym_suffix = c("_PP", "_NN"))

kardl_custom <- kardl(data = Seatbelts, my_formula)

kardl_custom## Optimal lags for each variable ( AIC ):

##

## DriversKilled: 1, asyP_PetrolPrice_PP: 0, asyN_PetrolPrice_NN: 0, asyP_drivers_PP: 2, asyN_drivers_NN: 0

##

##

## Call:

## lm(formula = my_formula, data = model_data)

##

## Coefficients:

## (Intercept) L1.DriversKilled L1.asyP_PetrolPrice_PP

## 123.16543 -1.02076 -64.65463

## L1.asyN_PetrolPrice_NN L1.asyP_drivers_PP L1.asyN_drivers_NN

## -67.68843 0.07313 0.07991

## L1.d.DriversKilled L0.d.asyP_PetrolPrice_PP L0.d.asyN_PetrolPrice_NN

## 0.07062 -314.39843 805.57820

## L0.d.asyP_drivers_PP L1.d.asyP_drivers_PP L2.d.asyP_drivers_PP

## 0.07503 0.01619 -0.01497

## L0.d.asyN_drivers_NN law trend

## 0.07760 -0.99053 0.63124Key Functions and Parameters

-

kardl(data, model, maxlag, mode, ...):-

data: A time series dataset (e.g., a data frame with DriversKilled, PetrolPrice, drivers). -

formula: A formula specifying the long-run equation, e.g.,y ~ x + z + asymmetric(z) + lasymmetric(x2 + x3) + sasymmetric(x3 + x4) + deterministic(dummy1 + dummy2) + trend. Supports:-

asymmetric(): asymmetric effects for both short- and long-run dynamics. -

lasymmetric(): Long-run asymmetric variables. -

sasymmetric(): Short-run asymmetric variables. -

deterministic(): Fixed dummy variables. -

trend: Linear time trend.

-

-

maxlag: Maximum number of lags (default: 4). Use smaller values (e.g., 2) for small datasets, larger values (e.g., 8) for long-term dependencies. -

mode: Estimation mode:-

"quick": Verbose output for interactive use. -

"grid": Verbose output with lag optimization. -

"grid_custom": Silent, efficient execution. - User-defined vector (e.g.,

c(1, 2, 4, 5)orc(DriversKilled = 2, PetrolPrice_POS = 3, PetrolPrice_NEG = 1, drivers = 3)).

-

- Returns a list with components:

inputs,finalModel,start_time,end_time,properLag,time_span,opt_lag,lag_criteria,type(“kardlmodel”).

-

kardl_set(...): Configures options likecriterion(AIC, BIC, AICc, HQ),different_asym_lag,asym_prefix,Sasymuffix,short_coef, andlong_coef. Usekardl_get()to retrieve settings andkardl_reset()to restore defaults.kardl_longrun(model): Calculates standardized long-run coefficients, returningtype(“kardl_longrun”),coef,delta_se,results, andstarsDesc.symmetrytest(model): Performs Wald tests for short- and long-run asymmetry, returningLhypotheses,Lwald,Shypotheses,Swald, andtype(“symmetrytest”).pssf(model, case, signif_level): Performs the Pesaran, Shin, and Smith F Bound test for cointegration, supporting cases 1–5 and significance levels (“auto”, 0.01, 0.025, 0.05, 0.1, 0.10).psst(model, case, signif_level): Performs the PSS t Bound test, focusing on the lagged dependent variable’s coefficient.narayan(model, case, signif_level): Conducts the Narayan test for cointegration, optimized for small samples (cases 2–5).ecm(data, model, maxlag, mode, ...): Conducts the Restricted ECM test for cointegration, with similar parameters tokardl()and case/significance level options.

For detailed documentation, use ?kardl,

?kardl_set, ?kardl_longrun,

?symmetrytest, ?pssf, ?psst,

?narayan, or ?ecm.

Conclusion

The kardl package is a versatile tool for econometric

analysis, offering robust support for symmetric and asymmetric

ARDL/NARDL modeling, cointegration tests, stability diagnostics, and

heteroskedasticity checks. Its flexible formula specification, lag

optimization, and support for parallel processing make it ideal for

studying complex economic relationships. For more information, visit https://github.com/karamelikli/kardl

or contact the authors at hakperest@gmail.com.